Homemaking is often described through visible work. Cooking, cleaning, decorating, organizing and caring for family members usually come to mind first. Yet a well-run home also depends on less visible work. Someone has to track bills, plan grocery spending, prepare for repairs and make sure money is available when the household needs it.

That is where a checking account becomes more than a basic banking tool. It can help organize the flow of household money. When the right account setup is paired with simple habits, homemaking becomes easier to manage because the financial side of the home is clearer.

Homemaking Includes Financial Organization

Every home has a rhythm. Groceries are bought weekly. Utility bills arrive monthly. Rent or mortgage payments have fixed due dates. Insurance, childcare, transportation, repairs and household supplies all need room in the budget.

These expenses can feel ordinary, but they add up quickly. A few small purchases at the store, an unexpected school fee or a higher electric bill can throw off the month if there is no system in place.

A checking account often shows this rhythm better than any other financial tool. Income comes in. Bills go out. Debit card purchases show what the household is using day to day. Transfers show what is being saved or moved for future needs.

This is also why people should look beyond surface-level incentives when choosing an account. Bank bonus offers can be worth reviewing, especially when the requirements are clear, but they should not be the only factor. A household-friendly account should also make it easy to track spending, understand fees, access funds and manage deposits. Some offers depend on eligible direct deposit activity and other terms, so reading the details matters before opening an account.

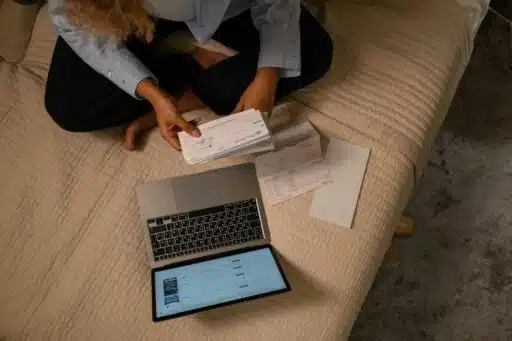

A Better Checking Account Can Make Bills Easier to Manage

Household bills are easier to handle when they are visible. A checking account can serve as the central place for recurring payments such as utilities, internet, phone service, insurance, rent, mortgage payments, subscriptions and childcare costs.

Automatic payments can help reduce missed bills. They are useful for busy households because they remove one task from the weekly list. Still, automatic payments need attention. A bill can clear earlier than expected. A subscription can renew without much warning. A payment amount can change.

That is why a bill calendar is useful. List due dates and match them to paydays or expected deposits. Then check the account weekly to confirm what has already cleared and what is still pending. This habit can prevent surprises and make sure enough money stays in checking before payments post.

Tracking Groceries and Household Spending

Groceries are one of the most flexible household expenses, which also makes them easy to underestimate. Prices change. Family needs change. A quick stop for milk can turn into a larger purchase. Several small trips can cost more than one planned shopping run.

Checking account activity can help reveal patterns. Reviewing debit card transactions may show how often the household shops, where money is going and which categories need more structure. Food, cleaning products, personal care items and home supplies may all appear in the same store purchases, so it helps to look at totals over time.

A realistic spending rhythm matters more than a perfect one. Some families do better with a weekly grocery amount. Others prefer a monthly household budget that includes food, toiletries and cleaning supplies. The goal is not to make every purchase rigid. It is to make spending visible enough to guide better choices.

Digital Banking Tools that Help Keep the Home Organized

Digital banking features can be practical tools for homemaking. Low-balance alerts can warn a household before spending moves too close to the edge. Transaction alerts can show when purchases happen and help catch errors. Deposit alerts can confirm when income, refunds or reimbursements arrive.

Mobile check deposit can also be useful. Even though many payments are digital, households may still receive paper checks from refunds, gifts, rebates or reimbursements. Being able to deposit a check from home saves time and keeps money moving.

Easy transfers help too. A household may move money from checking to savings for repairs, holidays or large purchases. Or it may move money back into checking when an unexpected cost appears. The smoother that process is, the easier it is to manage the home without extra stress.

Separating Household Money from Personal Spending

Some households benefit from a dedicated checking account for shared home expenses. This can be useful for couples, roommates or families where more than one person contributes to bills.

A separate household account can be used for rent or mortgage payments, utilities, groceries, childcare, repairs and shared subscriptions. Personal spending stays elsewhere. This makes it easier to see what the home costs each month.

The system should stay simple. Decide which expenses belong to the household account. Agree on contribution amounts. Review spending regularly. Too many rules can make the system hard to maintain, but a few clear boundaries can reduce confusion.

Planning for Repairs and Seasonal Costs

Not every home expense is monthly. Repairs, appliance replacements, holiday hosting, back-to-school shopping, seasonal utility changes, yard care and home projects often arrive at uneven times.

These costs can feel like emergencies when there is no money set aside. A checking account can help support a simple savings routine. After income arrives, transfer a set amount into savings for future household needs. Some people call these sinking funds. The name matters less than the habit.

Review last year’s irregular costs if possible. Look at repairs, seasonal spending and major household purchases. Then divide those costs into smaller monthly amounts. This makes large expenses less disruptive when they appear.

Making Family Spending More Visible

A clear checking account routine can also improve communication. In a shared household, both partners or decision-makers should understand which bills have been paid, what is coming up and how much is available for flexible spending.

This reduces repeated questions and helps avoid duplicate purchases. It can also support simple money conversations with older children. Parents can explain that grocery budgets, utility bills and savings goals are part of how a home works.

Money does not need to become a constant topic. But regular visibility can prevent misunderstandings.

What to Look for In a Household-Friendly Checking Account

A household-friendly checking account should be simple, affordable and easy to use. Low or no monthly fees can help protect the budget. Clear account terms are important too. Review overdraft policies, deposit timing, transfer limits, ATM access and support options.

Digital tools matter because home management often happens in small moments. A useful mobile app, account alerts, easy transfers, mobile deposit, debit card controls and clear transaction history can all make daily money tasks easier.

ATM and debit card access should also fit real household routines. Groceries, errands and unexpected purchases often happen away from home. Access should be convenient and secure.

A Simple Checking Account Routine for Homemakers

A weekly review can make a major difference. Check the balance. Review recent transactions. Confirm upcoming bills. Adjust grocery or household spending if needed.

Once a month, look more closely. Compare planned spending with actual spending. Review recurring charges. Cancel anything no longer needed. Plan for known expenses in the next month.

Every few months, reset the system. Look at seasonal costs, update savings goals and check whether the account still fits the household’s needs. A home changes over time. The money system should change with it.

Final Thoughts

Homemaking includes more than caring for the physical space. It also includes caring for the systems that keep the household steady.

A better checking account will not run the home by itself. It will not make every bill smaller or every purchase predictable. But it can make the money side of homemaking easier to see and easier to manage. With clear tools, simple routines and steady attention, a checking account can support a calmer and more organized home.

Journalist Chloe Rivera studied at the University of Missouri and has covered mindful, stylish living since 2013. She joined us in 2025 to curate realistic routines, budget-friendly décor, and community stories that help readers craft balance without perfection pressure. When offline, Chloe volunteers at urban farms, photographs street style, and hosts weekend swap parties for preloved clothes and books in her neighborhood.